Wind 'gold mines'

GRAHAM STEWART, ANNI PIIRAINEN, KATE JOHANNESEN AND ADRIAN DE ANDRES TAKE A LOOK AT HOW TO FIND THE PERFECT SWEET SPOT FOR LOCATING OFFSHORE WIND SITES

By 2050, the Carbon Trust estimates that the UK alone could host up to 35GW of floating offshore wind (FOW).1 Floating wind still has a long way to go before it is commercially competitive against conventional fixed structures. Developers are therefore faced with a dilemma: costs will reduce as development increases but waiting around until costs come down could mean forfeiting the most promising locations to competitors.

With the launch of a new offshore wind leasing round in Scotland (Scotwind), which has a significant proportion of sites suitable for floating wind, alongside the UK government’s consultation on the next contract for difference (CfD) allocation round, where will this expanding capacity be installed?

The characteristics that are expected to define an ideal floating site can be grouped as:

- Resource – the site should have high wind speed to achieve high energy yield

- Transmission – annual offshore Transmission Network Use of System (TNUoS) costs should be as low as possible

- Installation – proximity to the coast and a grid connection point is important to reduce cable lengths

- Operations & maintenance – onshore substation for grid connection should also have enough available capacity for connection without triggering extensive reinforcements of the network

To compute and visualise the financial feasibility of fixed and floating offshore wind in UK waters, Xodus Group has developed a tool that incorporates geographical information systems (GIS)

with sophisticated levelised cost of energy (LCoE) modelling. This provides a high-level and holistic understanding of where the ideal ‘gold mine’ offshore floating wind locations are, and where a rush for investment and development is expected.

Location, location, location

The LCoE tool has many different applications. It can be used for early site identification, micro-siting, and to better POWERunderstand the competition between sites or projects within a leasing or CfD round.

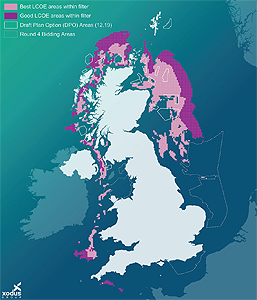

To understand where the most commercially lucrative areas for FOW development are located, the model was filtered to exclude fixed foundations, and by LCoE to include only the lowest values. The results shown in Figure 1 are based on a semi-submersible floating platform type, as this is the most progressed concept suited to a reasonably wide range of water depths. There will be some variation in the results if the model is applied to other floating platform types or specific designs The areas highlighted in light and dark pink have the lowest LCoE for FOW due to a more optimum balance being achieved across the range of parameters.

Developed through the analysis of more than 40 different calculated layers, the model’s CAPEX and OPEX estimations have been made through carefully overlaying these tiers. The pros and cons for each area have been summarised in Table 1.

The tool offers a purely techno-economic view of the potential for offshore wind development around the UK coastline. It is therefore a starting point in terms of the optimal development areas from an engineering perspective, prior to removal of any unsuitable areas due to the various constraints that may encountered. Evidently, the engineering and environmental considerations would need further analysis in tandem to ultimately select which sites would be most suitable for development, and to check compatability with the UK seabed leasing and consenting processes.

A floating future for wind power?

A notable takeaway from Figure 1 is the number of areas that are consistent with the locations of draft plan options (DPOs) currently under consideration for the upcoming ScotWind leasing round. As The Crown Estate has excluded water depths greater than 60m in Round 4, there is no overlap of the ‘gold mines’ with these zones in the map. However, the map highlights the potential suitability of additional areas outside of these zones for floating wind projects, which could be considered for inclusion in future leasing rounds. The tool is therefore well equipped to assist potential developers on determining the optimal areas within these DPOs/bidding areas to maximise revenue and minimise LCoE.

Careful consideration would therefore need to be given to the fundamental assumptions that make up each use-case. It is therefore recommended that the model and its filtering tool is re-run with tailored inputs to each specific project concept of interest to enhance the insights that can be gained.

As such, development of the LCoE GIS tool is not static and future versions will augment the model fidelity to include a greater range of built-in input options such as turbine size, project capacity, timeline and project technology considerations among others. This will facilitate direct comparison of a range of project options. Likewise, regional versions will also become available for the US

and Japanese offshore wind markets, for instance. An add-in module is currently under development to calculate the levelised cost of hydrogen for various project configurations as an alternative, or combined, route to market.

Within the Scotwind leasing round, significant emphasis will be placed on FOW due to the number of sites that would be uneconomic for fixed structures. A high level of developer interest is anticipated in a number of these areas and the expectation is that an increased push will be made to lower the LCoE of FOW in the upcoming years. The potential of a separate strike price for floating offshore wind in upcoming CfD rounds is therefore likely to accelerate this development, as well as any co-development and investment initiatives for floating wind coupled with the fledgling offshore hydrogen production industry.

Only the results of the leasing rounds will tell whether developers will take decisive action on this ‘gold fever’ for a more environmental and sustainable energy mix in the 21st century.

1 Carbon Trust, ‘Floating Offshore Wind: Market and Technology review’, June 2015

XODUS GROUP

Graham Stewart, Anni Piirainen, Kate Johannesen and Adrian de Andres all work at Xodus Group, a global energy consultancy, offering expert advice and solving complex problems. Multi-skilled specialists work across the energy spectrum providing advisory, engineering and consultancy services alongside intelligent data solutions.From concept and development, through consenting, asset management and optimisation to late-life and decommissioning, Xodus helps clients to maximise value, proactively seeking clever ways to do things better.

For further information please visit: www.xodusgroup.com